Effective tax planning can help you reduce your tax bill and claim little-known tax credits as well. In this article, we’re going to discuss year-end tax planning strategies that you can use in 2022.

Now, when I say “year-end tax planning”, that doesn’t mean that you wait throughout the year to try and sneak in a last-minute tax plan. As any tax professional will tell you, the best tax strategy is the one that you work toward throughout the year.

Here, we’re going to discuss several ways you can lower your tax bill. If you have questions about any of the tax strategies in this article, give us a call.

Our tax professionals and tax accountants can provide tax advice that’s tailored to your specific needs and situation.

3 Ways To Do Your Year-End Tax Planning

Tax planning at the end of the year helps to reduce taxable income for businesses and high-net-worth individuals. The past year has been especially hard and taxes can be an overwhelming burden. There are a few ways you can do your end-of-year tax planning:

Use tax software to do your year-end tax planning

Most taxpayers use tax calculators to estimate their tax liability and taxable income for federal taxes and local taxes at the end of the year. Tax calculators let you quickly estimate this year’s tax bill by inputting your estimates and projected numbers for this year.

Some common tax calculators are:

- SmartAsset’s Federal Income Tax Calculator

- IRS Tax Withholding Estimator

- HR Block’s Income Tax Calculator

Calculate your estimated tax bill using last year’s tax return

When you’re determining this year’s estimated tax bill, you’ll need to figure out your adjusted gross income, taxable income, deductions, and credits for the year. The IRS notes that you can use last year’s figures as a reference if you aren’t sure about this year.

To calculate your estimated taxes:

- Estimate your taxable income for this year

- Calculate your taxable income

- Calculate your self-employment tax

- Add these figures together and divide by four

Hire a tax professional for help with end-of-year tax planning

Getting the help of a tax professional or CPA will help you maximize your tax breaks and spot opportunities for deductible expenses that you may have missed. In addition to federal taxes, a tax accountant will also assist you with your state and local taxes.

There are different types of tax preparers. For example, you could pay tax preparation fees and enlist the help of enrolled agents or tax attorneys.

Enrolled agents can help you pay your local income taxes and federal taxes and help you spot local tax deductions. These tax professionals can provide tax advice to help you save tax dollars and take advantage of tax breaks.

For example, these tax professionals can help you figure out whether you’re in a higher or lower tax bracket, whether the standard deduction or itemized deductions are best, and whether you should make charitable contributions.

If you need legal advice related to your taxes, a tax attorney can provide legal advice in areas like trusts, estate taxes, and inheritance taxes.

Convert traditional IRAs into Roth IRAs

By converting a traditional IRA into a Roth IRA, taxpayers whose incomes have been very low in 2020 may be able to move the assets currently in their traditional IRA into a Roth IRA at a much lower tax rate.

Any amount can be converted, and with a little planning, the conversion tax can be low or even zero. To take advantage of this opportunity, the conversion must be made before year-end, and it is irrevocable.

Decide if you’ll itemize deductions or take the standard tax deduction

Individuals can itemize their deductions or take the standard deduction, which is $12,400 for singles and married couples filing separate returns, $24,800 for married couples filing jointly, and $18,650 for those filing as heads of household.

Because of the COVID-19 pandemic, some people have seen substantial reductions in their income, possibly so much so that their income may be less than their deductions, meaning they will not be taking full advantage of their deductions.

If you fall into that category, you should review your resources to determine if you have opportunities to increase your 2020 income to take full advantage of your deductions and cash in some income-tax-free states.

For example, you might be able to sell profitable stocks, withdraw funds from taxable retirement accounts (but only after age 59½ to avoid a penalty), or even exercise a stock option.

Make charitable contributions

If you are age 70½ or over and have an IRA, you can have your IRA trustee transfer IRA funds (up to $100,000) directly to a charity or charities of your choosing. Although the donation will not be tax-deductible, the distribution will not be taxable either, giving you an opportunity to help your favorite charity or charities with untaxed funds in this time of need.

Caution—the donation must be transferred directly from the IRA account to the charity; it cannot pass through your hands or it will be taxable.

2020 offers a variety of ways to make contributions, including donating unused time off from work (if your employer participates in the program). The AGI limitation for deducting cash contributions has been increased significantly, and non-itemizers can make a deductible contribution of up to $300 (pending legislation may change the amount).

Of course, a taxpayer over age 70½ can make an IRA-to-qualified charity donation. We can determine the method or combination of methods best suited to your particular circumstances.

Making an IRA-Qualified Charitable Distribution In 2022

Although the CARES Act suspended the required minimum distributions, this was not extended into 2021. In 2021, if you are 70 1/2 or older, you can make qualified charitable distributions of up to $100,000 in IRA assets without translating that distribution into your taxable income.

For 2022, a qualified charitable distribution must be reported on the 2022 federal income tax return. in early 2023, the IRA owner will receive a Form 1099-R that lists regular IRA distributions and qualified charitable distributions made during 2022.

Make traditional IRA contributions

The SECURE Act passed by Congress a little over a year ago removed the age restriction on making traditional IRA contributions beginning in 2020. Thus, taxpayers who are 70½ or older and still working are no longer prohibited from contributing to a traditional IRA. However, the contribution is still limited to earned income (income from working).

Traditional IRAs are tax-deductible, so consider whether you would gain any benefit from making a contribution for 2020. Plus, if you are not sure, you can defer the decision up to April 15, 2022, and still qualify for a 2020 tax deduction.

Adjust your marital status

Be mindful that filing status for the entire year is determined on the last day of the tax year, so no matter when you get married during the year, you will be considered married for the entire year for tax purposes. In addition, if a spouse is changing names, the Social Security Administration should be notified, and the IRS should be informed of any address change by either or both spouses.

If you are in the process of divorcing but the divorce isn’t final by December 31, the options for 2020 are for you and your spouse to file jointly or for you each to submit a return using the married filing separate status. There is an exception to this rule if a couple has been separated for all of the last 6 months of the year and one spouse has paid more than half the cost of maintaining a household for a qualified child.

In that situation, that spouse can use the more favorable head of household filing status. If each spouse meets the criteria for that exception, they can both file using the head of household status. Otherwise, the spouse who doesn’t qualify will need to use the status of married filing separately.

Those who are married filing jointly have less tax overall than filing two married separate returns, but when a joint return is filed, each spouse assumes liability for the full amount of the tax. This factor needs to be taken into account when determining the filing status of a married couple, especially when a divorce is in process or being contemplated.

If your divorce has been finalized and you haven’t remarried, your filing status will be single or, if you meet the requirements, head of household. Divorce creates numerous issues that can have profound implications on your tax return and the amount of your tax liability.

For example, who takes credit for the kids, allocating taxable income, who benefits from tax credits and deduction carryovers, alimony, and who is responsible for the tax liabilities are just a few issues to consider. It might be appropriate to project your tax liability in advance, so you can prepare for the outcome.

Take advantage of education tax credits

Both the lifetime learning education credit and the American opportunity credit allow qualified taxpayers to prepay 2021 college tuition bills for an academic period that begins by the end of March 2021. That means that if you are eligible to take the credit and you have not yet reached the 2020 maximum for qualified tuition and related expenses paid, you can bump up your 2020 credits by paying for 2021 now. This may not apply to you if you’ve been paying tuition expenses for the entire 2020 tax year, but if your child just started college this fall, it will probably provide you with some additional tax credit for 2020.

If you are a grandparent, you may be paying all or part of the tuition for a grandchild, and if the child’s parents are claiming the child as a dependent, then the parents receive the education credit if not phased out by the high-income limitation. If the payment is made directly to the college, there are no gift tax issues. So, the grandparent makes two gifts—tuition for the student and the tax credit to the student’s parents.

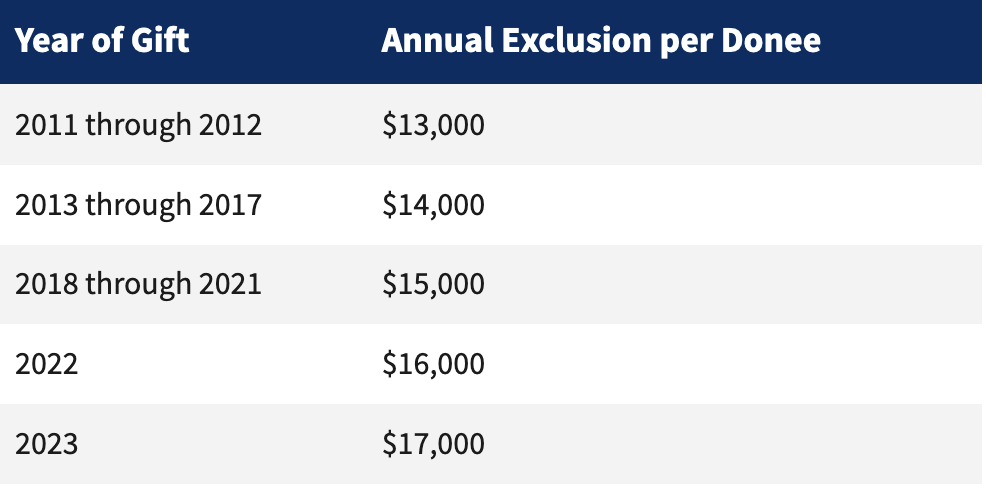

Use the annual gift tax exclusion

One of the best ways to reduce your taxes while giving to those you love is to take advantage of the annual gift tax exemption. Within specified limits, such gifts are not tax-deductible, which means you can give without having to pay any gift tax. If you want to do this, make sure that you do so by the end of the year, as you are not able to carry the gift amount into the next year. Here is an IRS table showing the gift tax exclusion limits for recent years:

Deduct unreimbursed medical expenses

If you’ve chosen to use itemized deductions, you are able to deduct unreimbursed medical expenses in excess of 7½ percent of your income (AGI). If you have reached that threshold or are close, it may make sense for you to pay off medical bills that are still outstanding rather than paying them over time.

If you are near or above the deduction limit, it may also make sense to look at what your expenses will be for the next year and move those that you can into 2020 to increase the deduction. These expenses could include dental work or eyeglasses.

Beware—if you are thinking of paying for those expenses using a credit card and you’re not going to pay the balance immediately, make sure that you’re not paying more in interest than you’re saving with the increased deduction.

Medical expenses charged to a credit card are counted toward your medical deduction for the year the expense was charged to the card, not as the balance on the card is paid off.

Sell declining stocks to offset capital gains

In a normal tax year, if you have stocks that have declined in value, you may wish to sell them before the end of the year and use the loss to offset other capital gains for the year or to produce a deductible loss. The net capital loss on a tax return that can be used to offset other types of income is limited to $3,000 for the year, but any excess loss carries over to future years.

You can repurchase the stocks you sold at a loss after 30 days have passed so you avoid the wash sale rules that prohibit a loss from being claimed when you repurchase the same or similar stock right away. However, (and depending on your overall situation), you may find yourself in a lower-than-normal tax bracket, and it actually may be beneficial to take stock gains rather than losses.

Also, be aware of the 0% income tax rate on long-term capital gains and qualified dividends from securities held other than retirement accounts. Yes, you could pay zero tax on long-term capital gains and qualified dividends if your taxable income is $40,000 or less. The upper limit for a married couple filing a joint return is $80,000, while it is $53,600 for those filing as head of household.

Avoid the tax penalty for having no health insurance

Although the federal government no longer penalizes individuals for not having minimum essential health insurance, some states do. The penalties can be a substantial amount of money and should be considered in end-of-year tax planning.

Consider using a donor-advised fund

If so, you might want to explore the benefits of donor-advised funds, which will allow you to make a large deductible charitable contribution this year and meet your future charitable obligations by distributing the funds in the upcoming years.

When you contribute cash and other assets to donor-advised funds, you are able to take a tax deduction. Note that the contributed funds cannot be returned to donors so you should consider your charitable contributions to a donor-advised fund as irrevocable.

Consider using a flexible spending account

These are valuable benefits because of the savings you can realize through pre-tax contributions, but only if you are making good use of them. You also want to check before the end of the year to see whether your plan allows any money left in your flexible spending account to be rolled over. If it can’t be, then you need to figure out how to spend it before the year is over, or else you’re just throwing money away.

Accelerate expenses

Accelerating expenses has been a great technique for businesses that use cash basis accounting, and it’s still usable under the TCJA. If you have expenses that you know you’ll need to invest in through the coming year, you can go ahead and make those purchases or pay those bills in advance before the end of December.

This allows you to add those expenses to the following year’s tax cycle. This is something to keep in mind because some of these deductions are not permanent changes, which means that they may not be available in the coming years.

Some companies will add these charges to an open line of credit to achieve the same goal. Still, there are limits to this approach, and you need to be meticulous in the bookkeeping if you’re paying the balance next year so you don’t accidentally try to deduct the same expenditure in subsequent years.

Consider buying cash-value life insurance

Purchasing a whole-life life insurance policy is a tax planning method that many use because it is tax-deferred. This allows your money to grow each year without being impacted by taxes every year. If you’ve set your policy correctly, your policy’s cash value can be accessed as a loan or withdrawal without any negative tax consequences.

Invest in index mutual funds and exchange-traded funds (ETFs)

There are several types of exchange-traded funds (ETFs), including bond ETFs and equity ETFs and others. ETFs are treated more favorably than mutual funds because they create and redeem through in-kind transactions which are not considered sales, which means they don’t create taxable events. If ETFs are part of your financial strategy, note that you must hold ETFs to receive long-term capital gains tax treatment. Otherwise, you will receive short-term capital gains tax treatment.

Distributions from mutual funds must be listed as investment income on your taxes each year. There are numerous factors to consider when you’re calculating how much income tax you’ll pay on your distributions, including:

- The type of distribution from the mutual funds

- The duration of your investment holding

- The type of investment

Often, distributions will be subjected to the ordinary income tax rate. In other cases, you may be able to lower your capital gains tax rate or receive tax-free distributions.

Invest in a Qualified Opportunity Fund (QOF)

Created under the Investing In Opportunity Act, Qualified Opportunity Funds (QOFs) offer tax incentives for those investing capital gains in economically distressed communities throughout America.

A Qualified Opportunity Fund (QOF) is an investment vehicle designed to invest in a Qualified Opportunity Zone property. There are two ways a QOF can be used:

- Investing in Opportunity Zone businesses that hold tangible property assets within Opportunity Zones

- Becoming a business within an Opportunity Zone by investing in tangible property that is located within the Opportunity Zone.

Click here to learn more about QOFs.

Consider tax-loss harvesting

If you’ve been an investor for any length of time, you’ve likely heard of tax-loss harvesting. Tax-loss harvesting helps investors reduce taxes owed on either capital gains or regular income by selling lost-value investments, replacing such investments with similar ones, then listing those sold investments as a loss to offset realized capital gains.

If you’re considering tax-loss harvesting, note that the IRS disallows investors from wash sales, which is when investors deduct losses from the sale of securities against capital gains of the same security.

Set up and contribute to a SEP-IRA or 401(k) account

One of the smartest ways to lower your taxable income is to contribute to a retirement account. Not only does doing so lower your business’s tax liability, but also ensures a more secure future. As a small business owner, either a 401(K) plan or a Simplified Employee Pension (SEP) plan will do the trick while benefiting both you and those who work for you in the future.

While a 401(k) that is established prior to year-end will let you deduct any contributions you make (with contributions limited to the lower of $57,000 or the employee’s total compensation), business owners who fail to set up this type of plan by December 31st can still turn to the SEP as an alternative.

Though SEP contributions are restricted to 25% of the business owner’s net profit less the SEP contribution itself (technically 20%), a SEP can be established, and contributions made up until the extended due date of your return. If you obtain an extension for filing your tax return, you have until the end of that extension period to deposit the contribution, regardless of when you actually file the return.

Use the Qualified Business Income (QBI) deduction (passthrough only)

One of the most impactful changes that the TCJA made for pass-through businesses whose income is passed through for taxation as their owners’ personal income is a valuable tax break known as the qualified business income (QBI) deduction. For those that are eligible, this deduction is worth a maximum 20% tax break on the income they receive from the business – but determining whether or not you are eligible can be a challenge.

There are several restrictions on taking advantage of the deduction, particularly with reference to specified service trade or businesses (SSTBs) whose owners either earn too much income or rely specifically on their employees’ or owners’ reputation or skill.

Though architecture and engineering firms escape this limitation, other business models – including medical practices, law firms, professional athletes and performing artists, financial advisors, investment managers, consulting firms, and accountants – fall into the category that loses out on the deduction if their income is too high.

In 2019, single business owners of SSTBs began phasing out at $160,700 and are excluded once their income exceeds $210,700, while those who are married filing a joint return phase out at $321,400 and are excluded at $421,400. To calculate the deduction, use Part II of Form 8995-A.

Businesses that are not SSTBs are eligible to take the deduction even when they pass the upper limits of the thresholds, but only for either half of the business owners’ share of the W-2 wages paid by the business or a quarter of those wages plus 2.5% of their share of qualified property.

These limitations and specifications for what type of business is and is not eligible are head-spinning, and though it is tempting to simply take the deduction, it’s a good idea to confirm whether you qualify and how to claim it with our office before moving forward.

Pay estimated tax payments early or on-time

If you are a sole proprietor or S corporation shareholder, you are required to pay estimated tax payments every quarter if you will owe $1,000 or more when you file your income tax return.

Making estimated tax payments on time or early will help you avoid tax penalties. In specific scenarios, the IRS provides penalty waivers.

Choose the right accounting method

Each small business owner calculates their income and revenue differently, with many using a method of accounting that is based on when money is received rather than when an order is placed and counts expenses when they are paid rather than the item or service ordered. This is known as the cash method of accounting.

Whatever method of accounting you use, smart business owners can strategically adjust their approach, reporting their annual income based on cash receipts in order to reduce their end-of-year revenues, especially if there is reason to believe that next year’s income will be lower or, for some other reason, they anticipate being in a lower tax bracket.

An example of how this approach would be helpful can be seen in the case of a business that expects to add new employees in the new year. Between that expense and other improvements planned, it makes sense to anticipate that net income will be down and the tax bracket for the business will be lower, so any work done or orders placed towards the end of the current tax year should be accounted for when payments arrive so that the income can be taxed at a lower rate.

The contrast to this is if you are anticipating your business revenue increasing and being forced into a higher tax bracket in the new year: in that case, it makes sense to try to collect monies for work done in the current year early, so that you can take advantage of your current, lower tax rate.

The same can be done for business expenses such as office supplies and equipment, which can be deferred and accelerated in the same way so that you can take advantage of tax deductions in the way that is most advantageous.

Restructure your business entity

When you started your business, one of the first decisions you needed to make was whether you wanted to operate as a sole proprietor, partnership, LLC, S corporation, or C corporation. But as more time goes by, the initial reasons for structuring your business the way that you did may no longer be applicable, or in your best interest from a tax perspective. There is no requirement that you stick with the business structure you initially chose.

The Tax Cuts and Jobs Act was such a large bill with so many implications that many businesses tried to make their current structure fit into the new laws with the best advantages possible. Now, it’s time to think proactively about using these regulations to your advantage and look for ways to decrease your tax liability and increase tax savings.

Ever since the Tax Cuts and Jobs Act of 2017 (TCJA) changed the highest corporate income tax rate from 35% to 21%, sole proprietorships, LLCs, partnerships, and S corporations can realize significant tax savings by electing to be taxed as a C corporation. This simple change can make sense if the owner of these pass-through businesses is taxed at a high tax bracket. If so, all you need to do is fill out and file Form 8832. Before doing so, make sure that the tax savings you can realize are a reasonable tradeoff for the other reasons that you may have originally selected the structure you are currently in.

That doesn’t necessarily mean that you should change structures. The advantages will still affect the decision on the type of structure your business currently is in versus the benefits of using a different structure. Pass-through business entities may be paying a higher tax percentage than C Corps, though they also can qualify for QBI deduction, which may offset the difference. Another thing to keep in mind here is the fact that deductions are limited for businesses that are not corporations, which may impact your bottom line.

Take advantage of relaxed Net Operating Losses (NOL) Limits

There is now an 80% limit on net operating loss. Before the TCJA, businesses could claim up to 100% net operating loss on taxable income, and they were able to carry back losses for up to two years. That’s changed.

Now you have a limit of 80%, and there is no longer the option to carry back losses to previous years. However, you can still carry forward losses to future years, and there is no limit on that option. Before the TCJA, there was a 20-year limit on carry-forward losses.

The TCJA simplified some accounting processes for businesses, but it also added a lot of changes that take some planning to take advantage of fully. That’s why it’s ideal if you look forward to fully use all of the deductions and benefits of this law before they expire. Year-end tax planning isn’t just about meeting the regulatory requirements. It should be about positioning your company for the best fiscal advantages moving into the new tax year.

Claim Employee Retention Credit (ERC Tax Credit)

Introduced as part of the CARES Act, the Employee Retention Credit provides financial relief to employers who kept employees on payroll during 2020 and 2021. The ERC is claimed through your quarterly payroll tax filing (Form 941) or an amended quarterly payroll tax filing (Form 941-X).

If you’d like to know more, get help with the ERC here.

Section 179 Accelerated Deductions

The Tax Cuts & Job Act changed the thresholds for Section 179 deductions, as well as the definition of qualifying property. The definition of qualifying property was expanded to include specific tangible property used for furnishing lodgings, as well as some upgrades to non-residential real property, like roofing and alarm systems.

Use Research & Development (R&D) Tax Credit

When you develop patents and create new products or software, you may be entitled to the Credit For Increasing Research Activities. You can learn more about this Research and Development credit.

Use Safe Harbor For PPP Loan Expenses Deductions In 2022

Many small businesses took advantage of the PPP loans that were offered by the government in the face of the COVID-19 crisis. While these loans were attractive because they are forgivable and gave businesses a chance to survive the dire circumstances, in April of 2020 the IRS issued Notice 2020-32, which indicated that despite the fact that the forgivable loans can be excluded from gross income, the expenses associated with the money received cannot be deducted. This effectively erases the tax benefit initially offered because losing the employee and expense deduction increases the business’ income and profitability.

There is some chance that this issue will be resolved by Congress, as it clearly contradicts the original intent of the tax benefit that accompanied the PPP funds, but that action has not yet been taken. It’s a good idea to talk to our office about this as soon as possible, as having to pay taxes on expenses incurred may be particularly challenging in the face of the difficulties the pandemic has imposed.

Being financially prepared to pay more taxes than you originally intended may be a bitter pill to swallow but will still be better than having to pay penalties and interest if you fail to pay what the government says that you owe.

Hire a tax professional and get year-end tax planning tips

As a full-service accounting firm, we provide tax services for our accounting and bookkeeping clients. Our team is highly skilled, experienced, and available for practical advice and informed guidance throughout the year. We believe that the best tax seasons are achieved through accurate accounting and bookkeeping – not a tax season “sprint.”